EMIR Clearing Clearer?

(Last updated: )

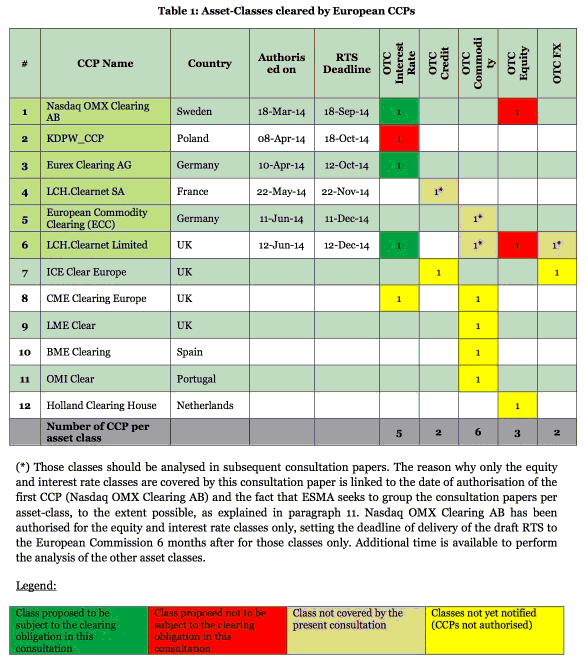

ESMA has launched two consultation papers examining the clearing obligation for IRS[1] and CDS[2]. Following the authorisation of six CCP’s[3], ESMA has grouped the consultation process into broad asset classes, each of which are assessed for their contribution to systemic risk and a consequent clearing mandate.

IRS: The RTS proposes the following four classes be subject to mandatory central clearing:

- Basis Swaps

- Fixed\Float interest rate swaps

- Forward rate agreements

- Overnight index swaps

CDS: The RTS proposes that European untranched Index CDS for two indices be subject to mandatory central clearing:

Single name CDS are (currently) excluded from the clearing obligation.

OTC Equities are not to be subject to the clearing mandate. Poland is (currently) excluded from the clearing obligation.

Application of the clearing mandate is to be phased-in according to counterparty classification (see below)

ESMA’s summary tables are reproduced below.

Interest Rate OTC derivatives

Basis swaps class

| Type | Reference Index | Settlement Currency | Maturity | Settlement Currency Type | Optionality | Notional Type |

| Basis | EURIBOR | EUR | 28D-50Y | Single currency | No | Constant or Variable |

| Basis | LIBOR | GBP | 28D-50Y | Single currency | No | Constant or Variable |

| Basis | LIBOR | JPY | 28D-30Y | Single currency | No | Constant or Variable |

| Basis | LIBOR | USD | 28D-50Y | Single currency | No | Constant or Variable |

Fixed-to-float interest rate swaps class

| Type | Reference Index | Settlement Currency | Maturity | Settlement Currency Type | Optionality | Notional Type |

| Fixed-to-Float | EURIBOR | EUR | 28D-50Y | Single currency | No | Constant or Variable |

| Fixed-to-Float | LIBOR | GBP | 28D-50Y | Single currency | No | Constant or Variable |

| Fixed-to-Float | LIBOR | JPY | 28D-30Y | Single currency | No | Constant or Variable |

| Fixed-to-Float | LIBOR | USD | 28D-50Y | Single currency | No | Constant or Variable |

Forward rate agreement class

| Type | Reference Index | Settlement Currency | Maturity | Settlement Currency Type | Optionality | Notional Type |

| FRA | EURIBOR | EUR | 3D-3Y | Single currency | No | Constant or Variable |

| FRA | LIBOR | GBP | 3D-3Y | Single currency | No | Constant or Variable |

| FRA | LIBOR | USD | 3D-3Y | Single currency | No | Constant or Variable |

Overnight index swaps class

| Type | Reference Index | Settlement Currency | Maturity | Settlement Currency Type | Optionality | Notional Type |

| OIS | EONIA | EUR | 7D-3Y | Single currency | No | Constant or Variable |

| OIS | Fed Funds | USD | 7D-3Y | Single currency | No | Constant or Variable |

| OIS | SONIA | GBP | 7D-3Y | Single currency | No | Constant or Variable |

Credit OTC derivatives

European untranched index CDS class

| Type | Sub-Type | Geographical Zone | Reference Index | Settlement Currency | Series | Maturity |

| Index CDS | Untranched Index | Europe | iTraxx Europe Main | EUR | 11 onwards | 5Y |

| Index CDS | Untranched Index | Europe | iTraxx Europe Crossover | EUR | 11 onwards | 5Y |

The standard criteria for inclusion in the clearing mandate account for the following factors:

- Standardisation- contractual terms and operational processes

- Liquidity- proportionate margins, stability of the market size and depth, market dispersion, number and value of transaction

- Availability of pricing information

Phased-in Application

- Category 1– clearing obligation applies 6 months after entry into force of the RTS

- Category 2– clearing obligation applies 18 months after entry into force of the RTS

- Category 3– clearing obligation applies 3 years after entry into force of the RTS

Note that 3rd country counterparties must assess their equivalent categorisation as if they were EU-domiciled. Counterparty classification is per the EMIR model-

| Case | FC | NFC+ that are not AIFs | NFC+ that are AIFs |

| Clearing Member meeting the conditions of Category 1 | Category 1RTS Article 2(1)(a) | Category 1RTS Article 2(1)(a) | Category 1RTS Article 2(1)(a) |

| Clearing Member NOT meeting the conditions of Category 1, or non-clearing members | Category 2RTS Article 2(1)(b)(i) | Category 3RTS Article 2(1)(c) | Category 2RTS Article 2(1)(b)(ii) |

[1] IRS account for 82.3% of outstanding OTC derivatives by notional amount. CDS account for 3.0%. Both figures are as of December 2013.

[2] Public consultation on draft technical standards is mandated by Regulation No 1095/2010.The two papers conform to the procedure laid down by ESMA/2011/BS/4a- including the proposed legal text of the RTS, an explanation of the measures and a cost-benefit analysis.

[3] The clearing obligation under Article 5(1) EMIR, is variously triggered by initial authorisation of a European CCP (Art. 14), an extension of a CCP’s activities (Art. 15), or ESMA’s recognition of a third-country CCP (Art. 25). Following any of these triggers, ESMA has six months to develop the applicable RTS.

3rd country counterparties must assess their equivalent categorisation as if they were EU-domiciled. Counterparty classification is per the EMIR model-

Contact Us