ISDA negotiations – the causes of delay, how you compare, and what you can do about it

(Last updated: )

ISDA negotiations – the causes of delay, how you compare, and what you can do about it.

Introduction

On 22 July 2024, ISDA published its latest “Digital Strategy Questionnaire”. The results of the survey provide a useful benchmark against which other market participants can measure their own performance in terms of trading document negotiation.

Who participated in the survey?

42 institutions participated in the survey – so it was quite a small sample size. The results probably shed more light on the activity of the sell-side than the buy-side, with 34 of the 42 respondents (80.95%) being either banks or broker-dealers. Two respondents (4.76% of the total) were institutional investors. There was also one government-sponsored bank and one supranational organisation.

Nonetheless, there was some representation from the buy-side, with one respondent from each of the following categories:

- corporate,

- hedge fund,

- insurance company, and

- mutual fund.

It’s also probably fair to say that the respondents tended towards the larger end of the market as nearly all stated that they are in scope for VM regulatory requirements (97.62%) and/or IM requirements (92.86%).

What does the average portfolio look like?

The profile of agreement portfolios of the survey respondents was probably fairly typical of most market participants.

56.00% of ISDA Master Agreements were 2002s, 39.00% were 1992s and 7.00% were 1992s that had been ‘upgraded’ (either bilaterally or through protocol adherence) to incorporate certain provisions from the 2002 (such as the Close-out Amount). Approximately 6% of the total were ‘deemed’ ISDAs (for example, through entry into a longform confirmation or adherence to the March 2013 DF Protocol).

Almost 90% of the ISDA Master Agreements were governed by either English law (50.01%) or New York law (39.74%). Only 0.36% were governed by French law and only 0.08% were governed by Irish law. Some other governing law accounted for 9.75% of the total.

How long does it take to negotiate a document?

At a high level, the results of the survey suggest that there is no significant difference between the timelines for negotiating an ISDA Master Agreement and a variation margin (VM) credit support annex (CSA). Unsurprisingly, the negotiation of an initial margin (IM) CSA and related documentation generally takes longer.

Looking at specific areas in more detail, 71.22% of negotiations involving ISDA Master Agreements and non-regulatory CSAs were completed within six months.

By comparison, 78.31% of VM CSA negotiations were completed within six months.

However, only 63.17% of IM CSA, account control agreement (ACAs) and eligible collateral schedule (ECSs) negotiation were completed within six months. Moreover, a significant minority (36.84%) of these negotiations last longer than six months versus 28.32% for ISDA Master Agreements and non-regulatory CSAs and 23.86% for VM CSAs.

Just over 11% (11.03% to be exact) of IM CSA, ACA and ECS negotiations took longer than one year. This was getting on for twice the rate applicable to VM CSA negotiations (6.57%). It was also almost three times more likely that a VM negotiation would be completed within one month (21.19%) compared to an IM CSA, ACA and ECS negotiation (7.22%).

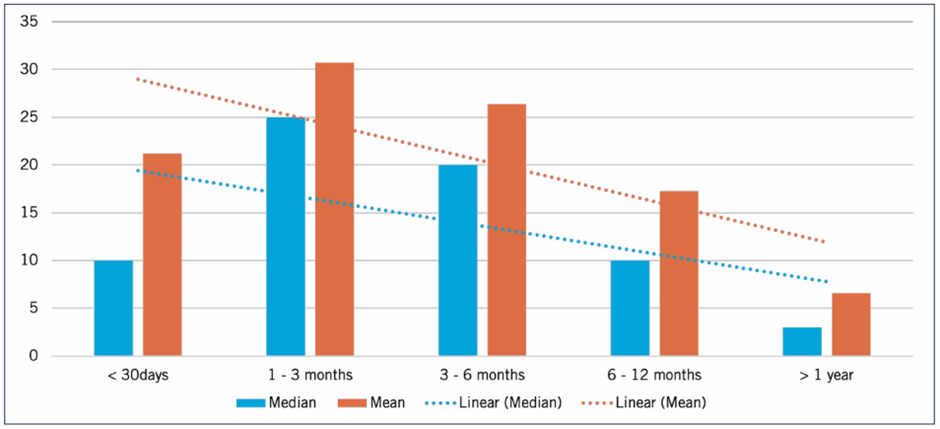

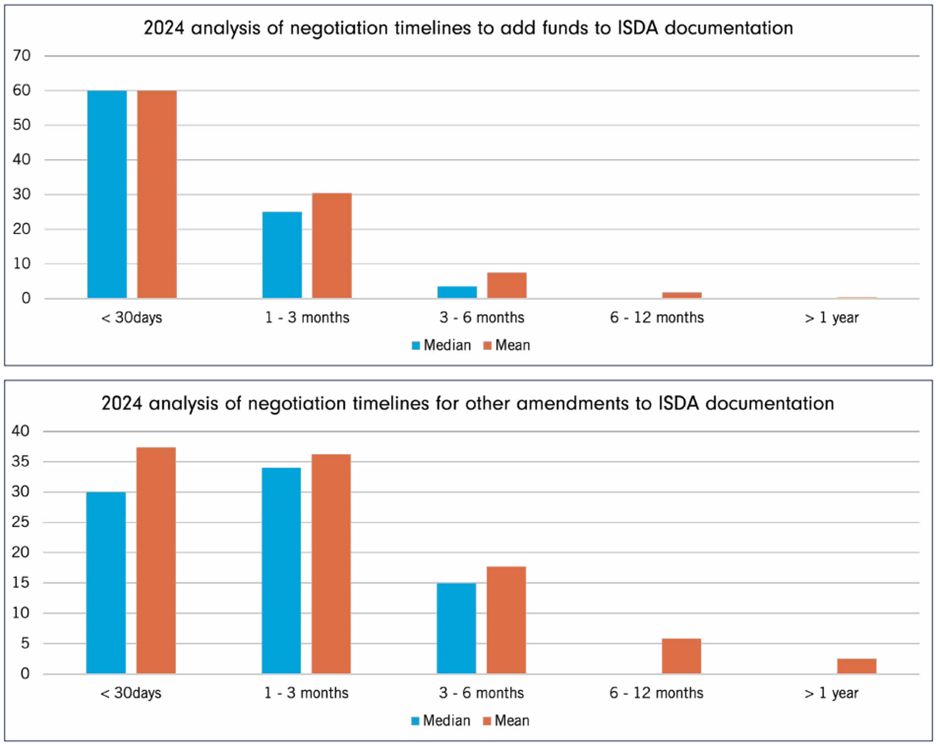

Unsurprisingly, general amendments and the addition of funds to ISDA documentation were significantly quicker to execute than the negotiation of ‘full blown’ documentation.

Rather worryingly, despite initiatives such as the ISDA Clause Library and despite the fact that negotiations now do really follow a very well-trodden path, the survey results suggested there has been NO IMPROVEMENT in negotiation times for ISDA Master Agreements and related credit support documentation since ISDA’s previous survey in 2006.

Why do negotiations get bogged down?

Unsurprisingly, the biggest cause of delay was counterparty responsiveness – cited by 92.86% of respondents (39 out of 42).

As one might expect, negotiation over particular provisions also causes delay. Additional termination events and credit-related issues were highlighted by over 60% of respondents. The complexities introduced by the requirement to segregate IM with a third-party custodian were mentioned by 65.79% of respondents (25 out of 38). Eligible collateral schedules have always been slow to negotiate and were cited as a source of delay in 60% of VM CSA negotiations and 47.37% of IM CSA negotiations.

As important as these factors are, to some degree, there are either uncontrollable or unavoidable. Of more strategic importance and relevance to the contract management process are those factors that CAN be controlled and/or avoided. On this front, lack of internal expertise and resources (both in terms of negotiation teams and internal approvers) were cited as causes of delay by 35.71% of respondents with respect to the ISDAs, 45.00% with respect to VM CSAs and 34.21% with respect to IM CSA)s.

What can you do about it?

So, even the biggest players admit that they don’t have the resources or the expertise needed for the task at hand task. Are you in the same boat?

The opportunity costs inherent in any delay are potentially significant. However, headcount freezes and/or lack of volume may make internal recruitment non-viable as a solution. Law firms can assist, but that is usually an expensive option.

But, if your delays are caused simply by a lack of resource or internal expertise, there is no need to suffer. The negotiation of trading documentation is what we do. We have the resources, the subject matter expertise, the language skills and the overall view of the market necessary to help you to plug the gaps and achieve your objectives – all at a price that makes sense.

Need a knowledgeable and professional service that is far more cost-effective than a law firm? Drop us a line at hello@drs-als.com.

Contact Us