Ring-fencing: the current state of play

(Last updated: )

Many senior financiers would describe the post-financial crisis architecture as brutalist and overpriced, with the plethora of regulations designed and implemented by a legion of legal bodies costing British banks billions over the last few years. As the deadline for ring-fencing is fast approaching, it seems opportune to assess the current state of the ring-fence build.

The banks’ expenditure to comply with regulations seems to be inexorable with ring-fencing in the wake of the notoriously colossal MIFID 2 which is estimated to total 1.4 million paragraphs. HSBC reported that in preparation for the legislation, they added 1,600 staff to their compliance team which now totals approximately 6,000, at a cost of £2.4 billion per annum. The cost of setting up the recently approved and ring-fenced HSBC UK will cost the bank £1.5 billion which equates to approximately 8.7% of its 2017 pre-tax profits.

The industry-wide cost of ring-fencing is estimated by analysts at Citi Group to be £7 billion.

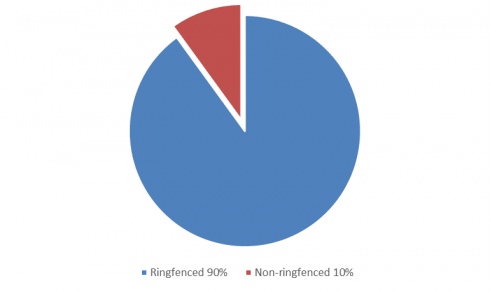

Ring-fencing applies to banks with more than £25 billion of consumer and SME deposits over a three year average. The Bank of England estimates that 75% of UK consumer banking deposits will be ring-fenced.

The Independent Commission on Banking published its final report in September 2011, in which it detailed what a ring-fenced bank (RFB) can and cannot provide in terms of services.

Once the bank has qualified for ring-fencing status, it then has to become:

- A separate legal entity.

- Operationally and economically separate, ensuring it is able to function efficiently regardless of the financial health of the rest of its group.

- Subject to loss absorbency measures, such as maintaining an addition ring-fence buffer of core equity tier 1 capital (CET1) above the Basel III baseline of 7%. The size of the capital buffer would depend on the size of the ring-fenced bank in relation to UK GDP (see table below).

[table id=3 /]

- RBFs are required to adhere to the mandatory and prohibited service guidelines as listed below.

Mandatory services

At this moment in time, the only services defined as mandated services are taking deposits from individuals and SMEs and providing overdrafts to individuals and SMEs, although the government has reserved the right to define additional mandatory services.

Prohibited Services

- Performing any service that would make it significantly inhibit any resolution action.

- Taking any risk which is not integral to the provision of payment services to customers.

- Providing any service to customers outside the EEA.

- Engaging in any service that involves exposure to non-ring fenced bank (NRFB) or a non-bank financial organisation. The exception to this is where, subject to prior regulatory approval, the exposure to a non-RBF/ non-bank financial organisation is associated with the provision of payment services. The RBF would also be able to transact with a non-RBF and other non-bank companies in respect of its ancillary activities.

- Provide any service which would result in a trading book asset.

- The purchase of derivatives or other contracts, requiring the RBF to hold regulatory capital against market risk.

- Services relating to secondary markets activity, including the purchase of loans or securities.

During a speech made at the British Bankers’ Association on the 16th of June 2017, James Proudman, the Executive Director for UK Deposit Takers Supervision, stated that “The Bank of England will require full and prompt implementation of the ring-fencing legislation and requirements by 2019” and appropriately went on to admit that “in short, there is a lot to be done”.

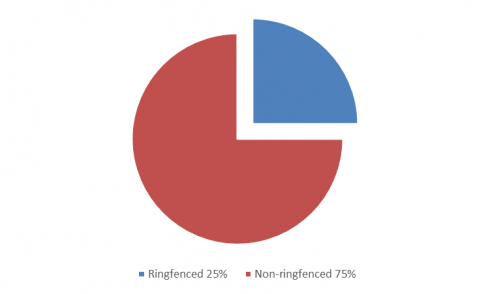

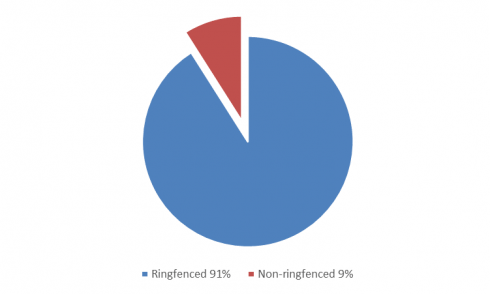

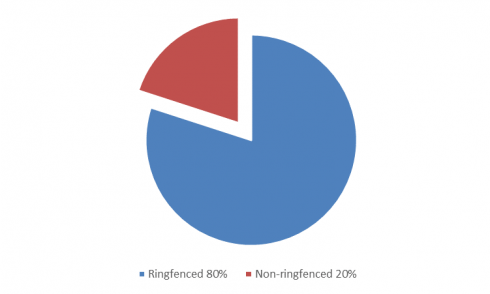

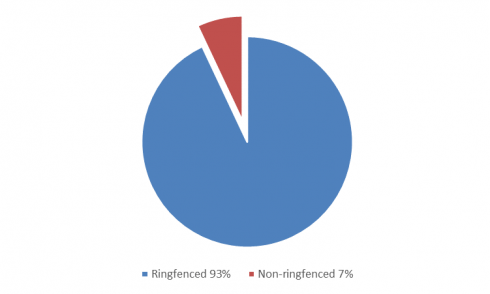

As per the below, the five banking groups’ distribution of group RWAs varies between their RFBs and NRFBs. At one end of the scale, heavily retail-focused Lloyds Banking Group, plans to hold just 7% of assets in its NRFB entities; at the other, Barclays will hold approx. 75% NRFB, reflecting its substantial trading, investment banking and large corporate businesses.

The charts below offer a simple summary of the current state of play.

Barclays

Risk-weighted assets

Following the High Court’s approval on 9th of March 2018 – Barclays became the first UK Bank to complete their investment banking separation. The newly formed Barclays Bank UK PLC (BBUKPLC) will provide day-to-day products and services to UK based individuals and SMEs with a turnover of less than £6.5m.

Inside the ring-fence (BBUKPLC):

- Personal and Premier Banking.

- Business Banking (SMEs)

- Barclaycard Personal UK.

- Wealth & Investments.

Outside the ring-fence:

- Barclaycard Business UK and Barclaycard Personal non-UK.

- Corporate Banking.

- Investment Bank.

- Private Bank & Overseas Services.

HSBC

The High Court approved HSBC’s proposal to move their personal customers and the majority of their business customers from HSBC Bank plc to HSBC UK on the 21st May 2018 and the bank has henceforth announced the 1st of July to be the scheduled transfer date.

Inside the ring-fence (HSBC UK):

- UK Retail Arms.

- First Direct.

- M&S Bank.

- UK Private Bank.

- UK Commercial Banking.

Outside the ring-fence:

- The Investment bank operations in Asia, the Americas and continental Europe.

RBS

RBS had announced that the ring-fencing of their retail banking operations would take place on the 30th April. The bank’s investment operation has been re-renamed as NatWest Markets, which along with its Jersey and Isle of Man bank; make up the 20% (following its post-2008 drastic diet) that is outside the ring-fence

Inside the ring-fence (NatWest Holdings):

- RBS.

- NatWest.

- Coutts.

- Ulster Bank.

Outside the ring-fence:

- NatWest Markets.

- Jersey and Isle of Man businesses.

Lloyds

Lloyds Banking Group (LBG) has set up Lloyds Bank Corporate Markets plc as their non-ring fenced bank and will continue to offer their personal and SME customers the majority of the products and services they offered pre ring-fencing from Lloyds Bank plc and Bank of Scotland plc.

Inside the ring-fence:

- Lloyds Bank plc.

- Halifax.

- Bank of Scotland.

Outside the ring-fence (Lloyds Bank Corporate Markets plc):

- Commercial Banking Markets Financing.

- Commercial Banking Financial Markets Products.

- Business undertaken by Lloyds Bank International in the U.S.A, Singapore and Crown Dependencies.

- Insurance, Lloyds Development Capital etc

Santander

Banco Santander has promulgated plans to use its London branch to house its UK corporate and investment banking activity outside of the ring-fence after the bank deemed creating two viable banks overly complex.

Inside the ring-fence (Santander UK):

- Retail.

- Vast majority of commercial and corporate.

Outside the ring-fence (Banco Santander):

- Complex trading such as derivatives.

- Operations based in Crown dependencies, such as Jersey and Guernsey.

Conclusion

Irrespective of cost, the utility and true value of the ring fence will only be assessed in the aftermath of the next crisis. Against the background of watered-down Volcker in the US and dead in the water Liikanen proposals in the EU, the UK will be the only major financial country with functional separation between investment banks and retail. UBS AG CEO Sergio Ermotti echoes many doubters, expressing his concern that capital constraints are making UK banks “too small to survive” instead of “too big to fail”. To our mind, this sounds like wishful thinking and in any event, is unlikely to keep taxpayers awake at night. More immediate concerns involve the deterioration and divergence of credit-ratings. While this may become more material than the current negative outlook, the banks’ holding companies will continue to issue the vast majority of their external debt, downstreamed to their operating companies in line with TLAC and UK MREL. Despite the fence’s many porous elements, the UK is to be congratulated for following through on its commitments, and at least to date, participant banks are to be admired for the relatively smooth implementation of a fundamental restructuring.

Contact Us