Indirect Clearing: In Search of One Template To Rule Them All

(Last updated: )

Background

EMIR introduced a clearing obligation in relation to “OTC derivative contracts” of any class that has been declared subject to a clearing obligation and which are transacted between particular types of counterparty[1]. MiFIR[2] extended the scope of the clearing obligation to all derivative transactions concluded on a regulated market. There are three basic ways in which a firm can satisfy the requirement to clear:

- by becoming a clearing member itself; or

- by becoming a client of a clearing member; or

- by establishing an indirect clearing arrangement with a clearing member[3].

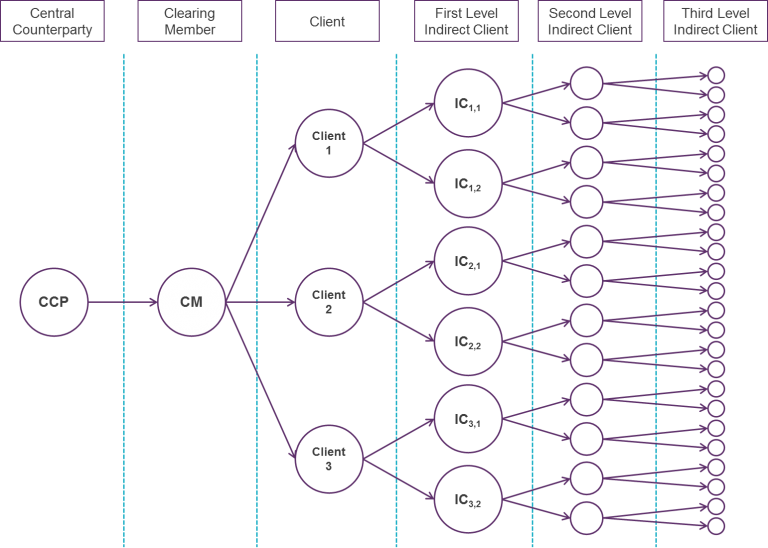

An “indirect clearing arrangement” is defined as “the set of contractual relationships between a central counterparty, a clearing member, the client of a clearing member and an indirect client, which arrangement allows the client of a clearing member to provide clearing services to an indirect client”. An “indirect client” is any undertaking which has a direct or indirect contractual relationship with a client of a clearing member (CM) which enables that undertaking to clear its transactions with a central counterparty (CCP).

There are no restrictions on the length of an indirect clearing ‘chain’ but longer chains, involving greater numbers of intermediaries, increases the complexity of indirect clearing arrangements. Nonetheless, if made available, both EMIR and MiFIR[4] require that indirect clearing arrangements do not increase counterparty risk and ensure that the assets and positions of the counterparty benefit from protections equivalent to those contained within Articles 39 (Segregation and portability) and 48 (Default Procedures) of EMIR for the indirect client at the end of the chain,[5] irrespective of the length of the chain or the jurisdiction of any entity forming a ‘link’ in the chain.

Broadly, Article 39 of EMIR requires CCPs and CMs to offer omnibus client segregation and individual client segregation to entities ‘one link down in the chain’ from themselves. They must also publicly disclose the levels of protection and costs associated with different levels of segregation that they provide.[6]

Article 48 of EMIR requires a CCP to:

- have in place procedures to deal with the default of a CM;[7]

- take prompt action to contain losses and liquidity pressures resulting from defaults;[8]

- take all reasonable steps to ensure that it can liquidate the proprietary positions of a defaulting CM and to transfer or liquidate client positions of the defaulting CM;[9]

- contractually commit to triggering porting procedures in relation to assets and positions held under omnibus client segregation structures[10] and individual client segregation structures;[11] and

- Effect ‘leapfrog payments’ to clients in relation to any balance owed by the CCP after completion of its default management process (unless the client to which the leapfrog payment is owed is not known to the CCP, whereby monies can be returned to the CM for the account of its clients).[12]

Under both EMIR and MiFIR, ESMA is tasked with developing draft regulatory technical standards specifying the types of indirect contractual arrangements that meet the above conditions.[13] The requirements for indirect clearing arrangements under EMIR were detailed in Commission Delegated Regulation No 149/2013 of 19 December 2012 (the EMIR RTS). On 28 September 2015, ESMA published draft technical standards with respect to MiFID II. However, draft RTS on indirect clearing under MiFIR were not published at this time, in recognition of the concerns raised during the course of public consultations relating to MiFIR. Instead, on 5 November 2015, ESMA published a Consultation paper on indirect clearing under EMIR and MiFIR, which remained open for comment until 17 December 2015

The Structure of Indirect Clearing

The consultation paper addressed three main topics:

- accounts structure and segregation models;

- default management requirements; and

- Longer chains.

ESMA detailed two indirect account structures within the consultation paper. The first would enable a client of a CM to distinguish its assets and positions from those of its indirect clients (an “omnibus indirect client account” or “OICA”). The second would not only enable a client of a CM to distinguish its assets and positions from those of its indirect clients, but would also enable the client to distinguish the positions and collateral value of each indirect client held within an omnibus indirect client account (a “gross omnibus indirect client account” or “GOICA”). The GOICA was presented as an alternative which provided all of the safeguards of the individually segregated indirect account (as detailed within the EMIR RTS) but without the associated administrative burden.

Under a GOICA structure margin must be transferred from the ‘end indirect client’ all the way up the ‘chain’ of indirect clearers to the CCP. It assumes that accounts and records are created up the length of the chain and requires that indirect clients are all identified. This enables the CCP to distinguish the collateral and positions held for the account of one indirect client from the collateral and positions held for the account of the “direct client” (i.e. the entity ‘next link up’ in the chain from the indirect client) or other indirect clients (i.e. those on the same level as the indirect client) and to calculate margin requirements separately for each indirect client – and so provide a level of protection equivalent to that of an individually segregated indirect clearing account[14]. Given that the identity of indirect clients would be known under a GOICA structure, the requirement to effect ‘leapfrog payments’ would remain. Note that this is not the case in relation to the OICA.

The chosen account structure – whether an OICA or a GOICA – impacts all parties in the indirect clearing chain. In a GOICA structure, CCPs require all necessary information on the collateral and positions held for the account of each indirect client in order to calculate associated margin calls on an indirect-client-by-indirect-client basis.[15] Similarly, a CM must ensure that the relevant CCP has all the necessary information to identify the positions and the collateral value held for the account of each indirect client in the GOICA on a daily basis.[16]

Irrespective of the underlying account structure, a CM must also establish effective default management procedures. The requirement to port remains, but has been downgraded to an “obligation of means” rather than an “obligation of results”. This means that CMs are only obliged to contractually commit to triggering procedures for the transfer (rather than guaranteeing the actual transfer) of assets and positions held by a defaulting client for the account of its indirect clients to another client designated by all of the indirect clients. Procedures for the prompt liquidation of the assets and positions of indirect clients following the default of the client (to be triggered in the event that the transfer to another client has not taken place within a predefined transfer period) must also exist. These must provide for the communication of information from the CM to indirect clients regarding the default of the client and the period of time during which the relevant indirect client portfolios will be liquidated.[17]

Moving further down the indirect clearing chain, any client of a CM which provides indirect clearing services must:

- provide the CM with sufficient information to identify, monitor and manage any risks arising from facilitating indirect clearing arrangements, including information on the number of entities involved in the indirect clearing arrangements and the jurisdictions of these entities;

- put arrangements in place so that, in the event of its default, all information held by it with respect of its indirect clients is made immediately available to the CM;

- in the event of its default, immediately provide the CM with sufficient information to identify the assets and positions of indirect clients;

- Present the indirect client with the new choice of account structures and make reasonable efforts to receive instructions from the indirect client on its choice of account and segregation model.[18]

Both any client and any indirect client which in turn provides indirect clearing services[19] (each, an “indirect clearer”) are subject to further requirements. Where the assets and positions of several indirect clients are managed within a GOICA the indirect clearer must:

- ensure that the relevant CM has all the information necessary to identify the positions and the collateral value held for the account of each indirect client on a daily basis; and

- Include, in its contractual arrangements with indirect clients, terms to facilitate the prompt return to the indirect client of the proceeds from the liquidation of the positions and assets held by the relevant CM for the account of the indirect client.

Irrespective of the underlying account structure, an indirect clearer must also:

- agree upon the contractual terms of an indirect clearing arrangement with its direct counterparties in the indirect clearing chain, after consultation with the CM on the aspects that can impact the operations of the CM;[20]

- request the CM to open a segregated account at the CCP for the exclusive purpose of holding the assets and positions of its indirect clients;

- disclose the details of the different levels of segregation and a description of the risk involved with the respective levels of segregation offered;

- provide the indirect client with sufficient information to identify the CCP and the CM used to clear the indirect client’s positions; and

- have the necessary arrangements in place to ensure that any liquidation proceeds received by the client for the account of one or more indirect clients does not form part of the client’s insolvent estate.

In Search of One Template to Rule Them All

Irrespective of the underlying account structure it is clear that, for an indirect clearing chain to operate effectively, information must flow smoothly both up and down the full length of the chain. All parties included in an indirect clearing arrangement are expected to share information so as to enable them to identify, monitor and manage any material risks arising from the arrangement,[21] including the length of the indirect clearing chain and the jurisdictions in which each intermediary is established. As the consultation paper states, “each intermediary should know their position in the chain, to which layer they correspond”[22]. This is particularly the case under the GOICA structure, under which each entity in the chain is responsible for making sure that information is exchanged[23] such that margin for each indirect client in the GOICA can be calculated separately and subsequently passed up[24] to, and then segregated at the level of, the CCP. In practice, the only way this can happen is if consistent contractual provisions exist between links in the indirect clearing chain.

It is equally clear that the efficient management of risk within an indirect clearing chain requires that all intermediaries be subject to largely identical contractual obligations. The requirement to ensure that indirect clearing does not increase counterparty risk and maintains equivalent levels of protection throughout the chain demands that consistent default management provisions apply throughout the chain and contractual arrangements which protect the amount owed to an indirect client in the event of the insolvency of any intermediary are established.

A healthy indirect clearing market is a key factor in the overall success of the central clearing model. However, central clearing generally, and indirect clearing in particular, still face a number of existential challenges. Chief among these is the capital intensive nature of the business, a factor which has forced a number of firms to reassess their approach to the entire question of clearing and calls into question the economic viability of the model. Regardless of the way in which these issues are ultimately resolved, one thing seems to be certain. Without standard documentation the indirect clearing initiative is doomed to failure. A single thread of an indirect clearing chain involves a highly complex series of operational interactions and information exchanges, all of which must function in a completely synchronous manner if regulatory compliance is to be achieved. The task becomes exponentially more difficult as both the length of the chain and the number of indirect clients increases. Ensuring contractual certainty along the length of cross-border indirect clearing chains will be particularly challenging. Without a single template documenting an agreed process around which the entire market congregates, it is difficult to see how the contracts of tens of thousands of market participant can be aligned – in terms of flow of information and default management – in a way that will comply with ESMA’s requirements. Industry bodies, such as ISDA and the FIA will undoubtedly look to take a lead in providing the tools the market requires. As OTC and ETD indirect clearing are, in many ways, merely different sides of the same coin, it is hoped that they will work together on the production of a single template, incorporating to the extent possible the (often) competing requirements of both buy- and sell-side participants. At this point, the market – recognising that its interests lie in compromise – must have the confidence to vote with its feet and back a single document.

[1] EMIR, Article 4(1)

[2] See Article 29(1)

[3] EMIR, Article 4(3)

[4] MiFIR, Article 30(1)

[5] Consultation Paper, paragraph 51, page 14

[6] Article 39(7)

[7] Article 48(1)

[8] Article 48(2)

[9] Article 48(4)

[10] Article 48(5)

[11] Article 48(6)

[12] Article 48(7)

[13] Article 4(4)

[14] See Article 3(2) of the draft RTS

[15] EMIR RTS, recital 7

[16] See Article 4(3) of the draft RTS

[17] RTS Article 4(7)

[18] EMIR RTS, recital 14

[19] See Article 5(1) of the draft RTS

[20] Article 2(2)

[21] EMIR RTS, recital 15

[22] Consultation Paper, paragraph 53, page 14

[23] Consultation Paper, paragraph 21, page 9

[24] EMIR RTS, recital 13

Contact Us