RIP TBTF? No

(Last updated: )

Mark Carney has today been widely misreported as hailing the imminent demise of TBTF. Announcing the consultation phase of the FSB’s Total Loss Absorbing Capital (TLAC) proposals, he said,

“Agreement on proposals for a common international standard on total loss-absorbing capacity for SIBs is a watershed in ending “too big to fail” for banks. Once implemented, these agreements will play important roles in enabling globally systemic banks to be resolved without recourse to public subsidy and without disruption to the wider financial system.”

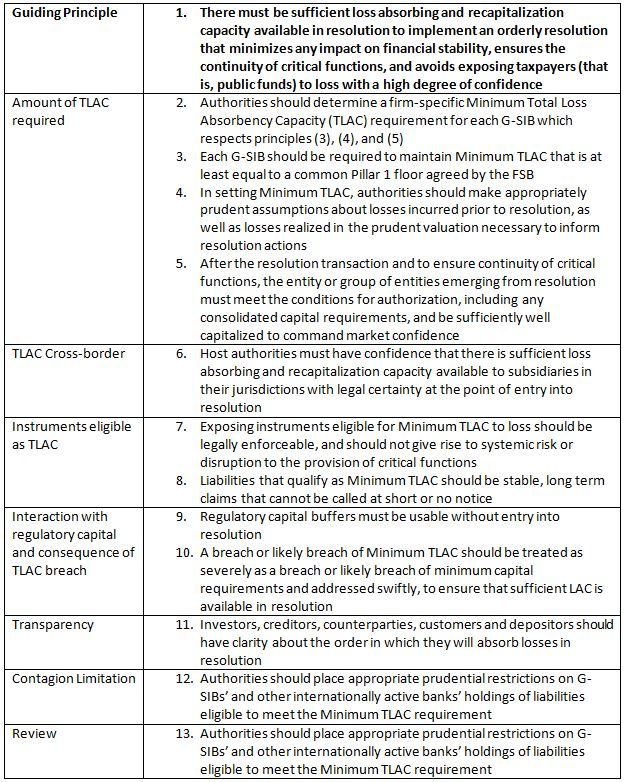

Firstly, the proposals haven’t been finalised (it’s a consultation); secondly, they haven’t been agreed; thirdly, the TLAC proposals may go some way to insulating the system from TBTF insolvency, but they do little for liquidity; fourthly, full implementation will only take place by 1 January 2019. Regulatory reform that truly ends TBTF would either explicitly break the G-SIB banks up into vastly smaller, more manageable units ,or would make the costs of implied subsidy so punitive that they would have no choice but to commit corporate hara-kiri. That said, a summary of the TLAC proposal follows:

- Applicable to the (currently) 30 G-SIBs

- Single specific minimum Pillar 1 TLAC to be set within 16-20% of RWA and at least X2 the Basel III leverage ratio. Final calibration to account for the consultation and a forthcoming Quantitative Impact Survey

- Specific TLAC numbers will take account of individual G-SIB RRPs, systemic footprints, risk profiles and organisational structures. The principles and term sheet provide guidance for national authorities to determine additional Pillar 2 TLAC requirement over the TLAC minimum

- An expectation that non-regulatory capital TLAC-eligible liabilities e.g. debt capital instruments will greater than or equal to 33&% of the Minimum Pillar 1 TLAC requirement

- TLAC should consist only of liabilities that can be effectively written down or converted into equity during resolution of a G-SIB without disrupting the provision of critical functions or giving rise to material risk of successful legal challenge or compensation claims

- A minimum TLAC requirement will apply to each resolution entity within each G-SIB and will be set in relation to the consolidated balance sheet of each resolution group

- Subsidiaries outside an entity’s home location which are identified as material but are not resolution entities, will be subj3ect to an internal TLAC requirement equivalent to 75%-90% of the stand-alone entity requirement

- Public disclosure of the amount, composition and maturity of TLAC is required as well as details of its postions in the creditor hierarchy

- To reduce contagion, holdings of other G-SIB’s TLAC will be deducted from a G-SIB’s own TLAC

Principles

The consultation paper includes a term sheet detailing the above principles. Both elements of the paper will be revised in the light of the consultation results and QIS, a final version will be submitted to the G20 by the 2015 Summit. The TLAC provisions will not apply before 1 January 2019.

Contact Us